The landscape of crypto taxation in Australia continues to evolve as more Australians engage with digital assets in 2026. Amid growing adoption, understanding how the Australian Taxation Office (ATO) classifies, taxes, and regulates cryptocurrency is crucial for anyone holding or trading assets such as Bitcoin, Ethereum, or emerging altcoins. The modern framework treats cryptocurrencies primarily as property, subjecting gains and income derived from crypto activities to capital gains tax (CGT) or ordinary income tax. Navigating the intricacies—like which transactions trigger taxable events, how to apply CGT discounts, and the reporting obligations—is essential to avoid costly penalties. Additionally, novel regulations such as the upcoming Crypto Asset Reporting Framework (CARF) are set to increase transparency and international data sharing, impacting how crypto tax compliance unfolds across borders. Whether you are a casual investor or an active trader, keeping abreast of 2026’s crypto tax laws in Australia ensures your financial strategy aligns with government requirements and maximizes tax efficiency.

Brief – Key Takeaways on Crypto Tax in Australia 2026:

- Cryptocurrencies are treated as property by the Australian Taxation Office and subject to capital gains tax or income tax depending on activity.

- Selling, trading, gifting, or using crypto as payment constitutes a taxable disposal event.

- A 50% CGT discount applies to assets held for more than 12 months by individuals, significantly reducing tax liability.

- Mining rewards, staking income, and airdrops are classified as ordinary income and taxed according to marginal rates plus a 2% Medicare levy.

- Taxpayers must maintain comprehensive records for at least five years, including cost base, disposal dates, and AUD valuations.

- Crypto-to-crypto trades are taxable, countering the misconception that gains are only realized when converting to Australian dollars.

- The implementation of CARF in 2027 will enhance data sharing between Australian and international tax authorities to improve compliance.

- Strict adherence to reporting and record-keeping helps avoid audits, penalties, and reassessments by the ATO.

Understanding the Core Framework of Crypto Taxation Australia 2026

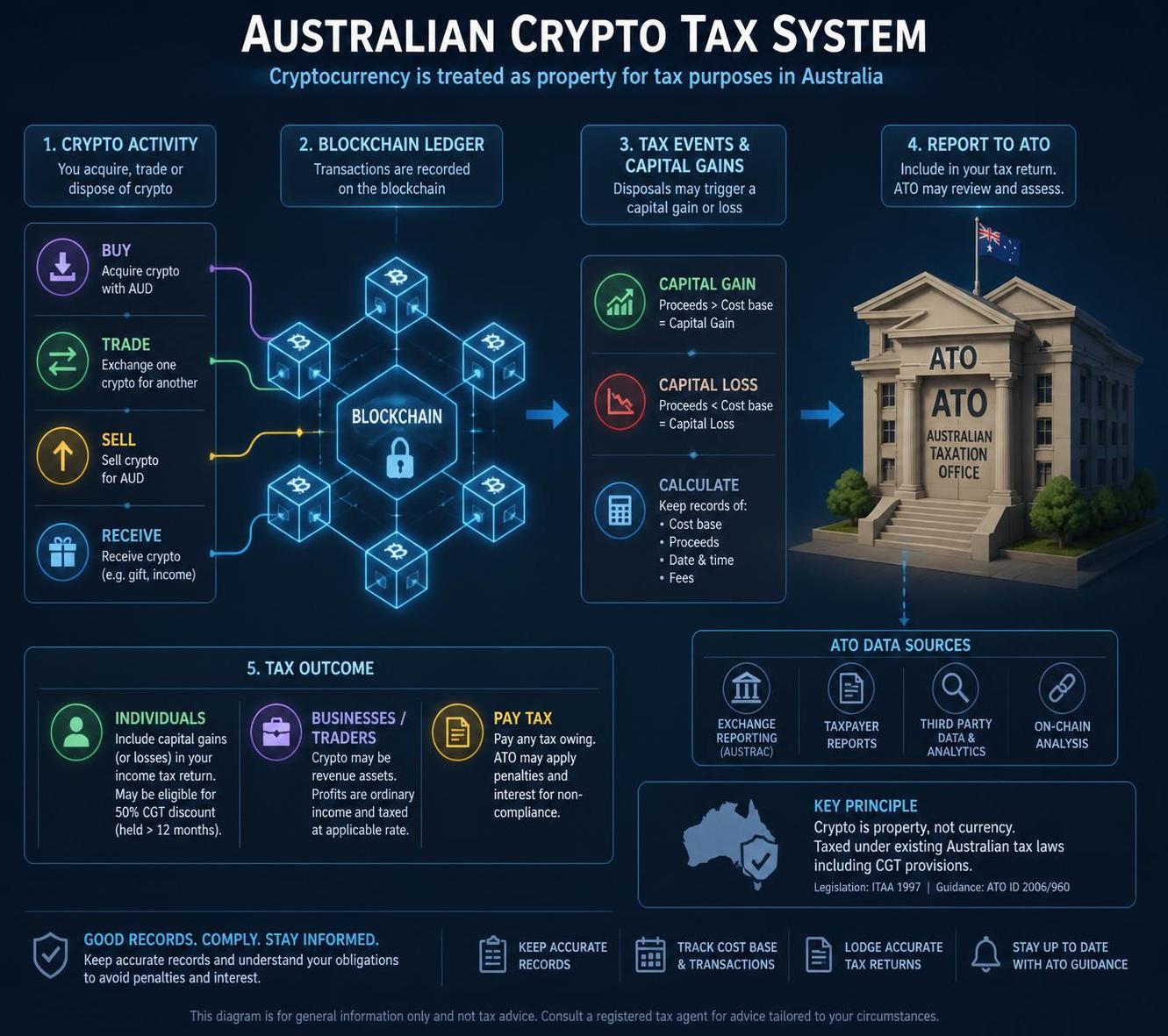

At its core, the Australian Taxation Office treats cryptocurrency as a form of property, similar to shares or real estate, which means that the cryptocurrency tax rules reflect capital gains tax principles combined with ordinary income assessments where appropriate. This dual approach dictates how various types of transactions and crypto-related income are taxed in 2026. For instance, if you sell your Bitcoin after holding it for some time, the transaction is classified as a CGT event. Conversely, income generated from activities like mining or staking is considered ordinary income and taxed accordingly.

This system means investors must be vigilant with every crypto transaction, whether it’s swapping Bitcoin for Ethereum or using crypto to purchase goods. Every instance of “disposal” is taxable. The calculation involves determining the difference between the cost base (what you originally paid) and the capital proceeds (market value at disposal). If the proceeds exceed the cost base, the difference qualifies as a capital gain. The opposite results in a capital loss, which can be useful to offset other capital gains the taxpayer has realized, thereby reducing the net tax liability.

This regime poses many practical questions: how are different crypto activities classified, what types of income need to be reported explicitly, and how can an individual minimize their tax burden legally? Understanding these nuances is vital to ensure compliance and efficient management of digital assets under Australia’s tax regulations crypto framework. For a more detailed guide on these principles, resources like coinixpro.com’s crypto tax Australia guide offer comprehensive insights tailored to investors and traders.

Detailed Analysis of Crypto Capital Gains Tax and Ordinary Income Tax in Australia

Australian tax law imposes distinct treatment for capital gains versus income from cryptocurrency. When disposing of crypto assets, capital gains tax is typically the main consideration. Capital gains in Australia are taxed at marginal income tax rates ranging from 0% up to 45%, plus the 2% Medicare levy. These rates align with standard individual income tax brackets. A key benefit in the Australian system is the 50% CGT discount for assets held over 12 months. This means if you keep your cryptocurrency for more than a year before selling or trading it, only half of your capital gain is added to your taxable income, effectively lowering the tax bill.

Below is a summary of the 2025-2026 individual income tax rates that apply to crypto-related capital gains and income:

| Taxable Income (AUD) | Tax Rate | Tax Payable |

|---|---|---|

| $0 – $18,200 | 0% | Nil |

| $18,201 – $45,000 | 16% | 16c for each $1 over $18,200 |

| $45,001 – $135,000 | 30% | $4,288 + 30c for each $1 over $45,000 |

| $135,001 – $190,000 | 37% | $31,288 + 37c for each $1 over $135,000 |

| $190,001 and over | 45% | $51,638 + 45c for each $1 over $190,000 |

Aside from capital gains, certain crypto earnings—such as rewards from mining, staking, airdrops, and lending—are categorized as ordinary income. Unlike capital gains, income tax on these earnings is calculated without the CGT discount. As such, these amounts are fully taxable in the year they are received, calculated at the individual’s marginal income tax rate plus the Medicare levy.

This distinction between capital gain and income tax nuances exemplifies the complexity of digital currency taxation. Implementing solid accounting practices and consulting reputable sources like the Your Income Calculator’s simple guide to cryptocurrency tax in Australia can help taxpayers manage their obligations effectively.

Comprehensive Breakdown of Taxable Events and Disposal Triggers in Crypto Transactions

One of the more intricate aspects of the crypto taxation Australia system is determining exactly when a taxable event occurs. Unlike traditional assets, crypto is frequently exchanged or converted, and each action may initiate a capital gains or income tax event under ATO guidelines.

Taxable events generally include:

- Selling crypto for fiat currency (e.g., AUD)

- Trading one cryptocurrency for another, such as swapping Bitcoin for Ethereum

- Using crypto to purchase goods or services—if the crypto exceeds the personal use asset exemption threshold

- Gifting cryptocurrency (except to a spouse in certain conditions)

A common misconception is that only cashed-out gains generate tax liabilities, but as illustrated, crypto-to-crypto trades are also reportable events, subject to capital gains tax. Calculating gains or losses in this context requires converting the AUD value of the assets at both acquisition and disposal times, which can become complex for frequent traders or DeFi participants.

It’s important to highlight the personal use asset exemption that applies if the cryptocurrency was acquired for less than $10,000 AUD and genuinely used for personal transactions in the short term. Such cases may not invoke CGT but are narrowly interpreted by the ATO and must be documented carefully to avoid misclassification.

For more details on the types of transactions and disposals considered taxable events, consult specialized resources such as CryptoTaxList’s 2026 Australia Crypto Tax Guide, which provide clear scenarios and examples for taxpayers.

Record-Keeping Requirements and Practical Tips for Tax Reporting Crypto Holdings

Maintaining meticulous records is foundational in managing your crypto tax reporting obligations to the Australian Taxation Office. The ATO requires that taxpayers keep records for at least five years after the relevant transaction occurs. These records must capture the necessary information to substantiate capital gains calculations or assess income properly.

Essential record elements include:

- Dates of acquisition and disposal of cryptocurrencies

- Value in Australian dollars (AUD) at times of acquisition and disposal using reliable exchange rates

- Details of the transaction counterparty, wallet addresses, and exchanges used

- The purpose of each transaction, especially to substantiate personal use asset exemptions

- Receipts for mining hardware or staking platforms relevant to income deductions

Given the complexity and volume of trades many investors undertake, leveraging tax software or professional crypto tax services can greatly reduce errors and improve compliance. The Australian ATO has sophisticated data-matching arrangements with exchanges, increasing the likelihood of discrepancies identified in tax returns on crypto transactions.

Tools and guides from platforms such as CoinTracking’s Australian tax guide help automate data organization by converting crypto movements into tax-ready reports. Adequate preparation avoids penalties and audits, underpinning a smoother tax filing experience.

Understanding Crypto Income Tax Elements: Mining, Staking, Airdrops, and NFTs

Distinct from capital gains, crypto income tax obligations arise when individuals receive new coins or tokens from network participation or promotional activities. Mining rewards are assessed as ordinary income at the market value upon receipt. Similarly, staking rewards—where investors lock crypto in blockchain protocols to support network functions—generate taxable income at the time tokens are distributed.

Airdrops and certain token distributions also fall under assessable income. The taxation timing is usually when the asset is received, with the fair market value determining the amount declared. For Non-Fungible Tokens (NFTs), each sale or swap qualifies as a disposal, triggering CGT events, while promotional NFTs provided are taxable on receipt as ordinary income.

Professional traders or businesses engaged in high-volume operations may be categorized differently, with income reported as business profits rather than personal capital gains. This designation changes the nature of deductibles and tax filing requirements significantly.

Given these complexities, seasoned investors often consult detailed publications like KuCoin’s 2026 crypto tax guide for best practices on reporting diversified crypto incomes.

Preparing and Lodging Your Australia Crypto Tax Return for 2026

Filing your crypto taxes successfully requires an accurate and thorough reporting of all capital gains and income derived from digital assets in the annual tax return. The Australian financial year ends on June 30, with self-preparers required to lodge by October 31, while agents have until May 15 to submit returns.

Taxpayers must include:

- Capital gains details scheduled in the CGT section of the tax return, specifying total gains and net gains after applying discounts or losses

- Crypto-derived ordinary income (from staking, mining, airdrops) declared under Other Income with accurate AUD valuations

- Deductions for any allowable expenses related to crypto business or income-producing activities

The ATO offers myTax online services for individual submissions, accompanied by detailed CGT schedules when necessary. With enhanced exchange data reporting and CARF implementation on the horizon, the expectation for transparent and detailed reporting will only increase.

Effective tax management also means considering PAYG (Pay As You Go) installment requirements if sizable gains or income are anticipated. Setting aside funds periodically to cover tax liabilities prevents liquidity issues at fiscal year-end. More guidance for Australian crypto taxpayers on filing techniques can be accessed via reliable resources such as dTax’s crypto tax guide Australia 2026.

Navigating the Future: CARF and International Crypto Tax Compliance in Australia

The forthcoming Crypto Asset Reporting Framework (CARF), expected to be introduced in Australia in 2027, represents a pivotal shift in crypto tax compliance. CARF will require exchanges and platforms to share comprehensive transaction data not only with the Australian Taxation Office but also with overseas tax agencies under international agreements. This development aims to curb tax evasion by creating greater transparency across jurisdictions.

By 2028, Australian taxpayers engaged with global exchanges will face heightened scrutiny, making accurate reporting of all crypto income and gains across borders imperative. This transformation intensifies the need for diligent record-keeping and compliance throughout 2026 and beyond.

The Australian government’s proactive stance means that crypto holders who neglect their tax reporting crypto obligations risk audits, penalties, and interest charges on unpaid taxes. Staying informed through trusted channels and adapting compliance strategies early will position crypto investors advantageously as the regulatory landscape tightens.

Strategies for Minimizing Australian Crypto Taxes Within Legal Boundaries

As Australia’s crypto tax laws grow increasingly sophisticated, investors are also exploring legitimate strategies to optimize their tax positions. One effective approach is leveraging the 12-month rule to access the 50% CGT discount. Holding assets longer can substantially reduce taxable capital gains from crypto trading.

Additionally, managing losses through strategic disposals can offset gains elsewhere, reducing overall tax liability. Investors might also consider tax-efficient timing for converting or utilizing crypto assets, aligning with their broader income and tax bracket considerations.

For active traders or businesses, precise tracking of income-producing expenses—such as mining hardware costs, transaction fees, or staking platform charges—can translate into deductible expenses that lower taxable income.

Innovative software tools that reconcile trading history and provide detailed reports compliant with Australian tax regulations become invaluable for maintaining accuracy and maximizing tax benefits. Resources like CoinLedger’s crypto tax guide help Australians navigate these opportunities while staying within legal frameworks.

Is trading one cryptocurrency for another taxable in Australia?

Yes, crypto-to-crypto trades are considered taxable capital gains events. You must calculate gains or losses based on the AUD market value difference at the time of the trade.

What is the benefit of holding crypto for more than 12 months?

Holding crypto for over 12 months enables a 50% capital gains tax discount for individuals, halving the taxable gain amount.

Do I owe tax if I just hold crypto without selling?

No tax is due while simply holding crypto. Taxable events occur only upon disposal, such as selling, trading, gifting, or using crypto for payments.

How should I report staking rewards for tax purposes?

Staking rewards are treated as ordinary income and should be reported at their fair market value in AUD when received.

Can I claim a capital loss if my crypto is lost or stolen?

You may be eligible to claim a capital loss if you have evidence of loss or theft, provided you can substantiate ownership and the loss to the ATO.